Filed under: Investing

In another blow to the coal industry, the Environmental Protection Agency, recently announced rules demanding that power plants should reduce carbon emissions by 30% from 2005 levels by 2030. The likely effect of enacting these rules will be to damage prospects for U.S. coal miners, and with China increasingly concerned with reducing its dependence on coal, their (coal miners’) export prospects could also be adversely affected in the future. With that said, it’s time to look at which companies have upside and downside opportunities if the “war on coal” continues.

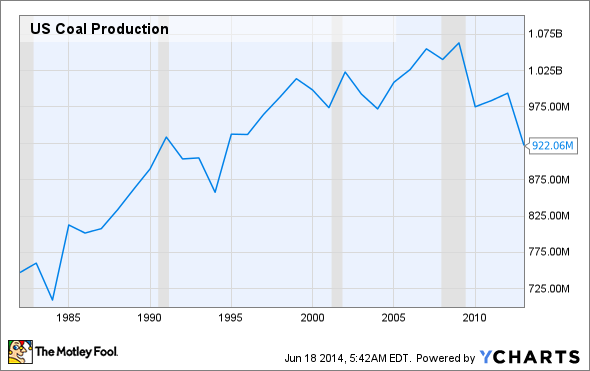

False dawn for coal mining?

You don’t need to be Einstein to understand the importance of relativity, and the fact that Joy Global‘s management recently predicted U.S. coal production would be incrementally positive this year is obviously a short-term positive.

However, it’s far too early to conclude that coal has passed an inflexion point on the way to another multi-year expansion. For example, Caterpillar recently lowered its forecast for full-year resource industry sales from a negative 10% to a negative 20%. Caterpillar’s stock price is doing well this year, but it’s more about the construction sector exceeding expectations and successful implementation of manufacturing cost reductions.

In addition, A quick look at U.S. coal production over the last 30 years demonstrates the demise of coal in recent years. Moreover, Fools should note that the extent of the period of decline since the last recession indicates that this isn’t just an adjustment to a slowdown in global growth.

US Coal Production data by YCharts.

Joy Global’s response to these difficulties is to initiate programs in order to increase its service-based revenue — a worthy plan, but hardly indicative of a strong end market for coal mining capital machinery. In addition, there are increasing question marks over China’s fixed-asset investment program, and therefore demand for key commodities like iron ore. Speculators already fear more defaults in China after an investment product linked to a coal miner, Liansheng Resources, defaulted earlier this year. Add in China’s move to bring forward the reduction in the percentage of its energy production from coal, another blow to the coal industry, and the outlook is uncertain at best.

While Joy Global and Caterpillar have an obvious exposure, the railway companies are also exposed because coal carloads make up a significant part of rail traffic in the U.S.

General Electric and Emerson Electric — set to do well?

While some companies are likely to suffer if coal continues to decline in importance, others could be set to do well. General Electric and Emerson Electric spring to mind, because three sub-sectors of the industrial economy are likely to flourish in the coming years:

- Increased natural gas production as gas replaces coal because of regulatory issues, is likely to spur ongoing investment in shale gas technology.

- Increased usage of gas turbines for power production will create additional service revenue growth.

- The increase in natural gas usage should create downstream opportunities for process technology solutions.

Although, General Electric and Emerson Electric both have revenue tied to coal — an inevitable consequence of its historical importance to power generation — they both have upside to these three factors. For example, General Electric has invested heavily in restructuring its oil and gas segment toward growth areas like shale gas technology. Moreover, General Electric’s gas turbine operations remain one of its single biggest profit drivers. In fact, gas turbines are so attractive, Siemens has now stepped in and made an offer for Alstom’s gas turbine business in a bid to that could derail General Electric’s offer for Alstom’s energy business.

As for Emerson Electric, the company is broadly diversified, but its biggest segment is process management, and it has growth opportunities from increased investment in downstream process technology in areas like chemicals and power. As the U.S. seeks to reduce its dependence on foreign energy, while also cutting carbon emissions, the outlook for the natural gas production will only get better — a byproduct being that process technology solution providers like Emerson Electric will do well.

The bottom line

The difficulties faced by the coal industry in the future will be felt by the coal miners and mining machinery companies like Caterpillar and Joy Global. In addition, railway companies are somewhat exposed, too. However, it’s not all doom and gloom, companies like General Electric and Emerson Electric look set to do well out from the U.S. energy boom. Fools would be smart to follow these trends.

OPEC is absolutely terrified of this game-changer

Imagine a company that rents a very specific and valuable piece of machinery for $41,000 per hour (That’s almost as much as the average American makes in a year!). And Warren Buffett is so confident in this company’s can’t-live-without-it business model, he just loaded up on 8.8 million shares. An exclusive, brand-new Motley Fool report reveals the company we’re calling OPEC’s Worst Nightmare. Just click HERE to uncover the name of this industry-leading stock… and join Buffett in his quest for a veritable landslide of profits!

var FoolAnalyticsData = FoolAnalyticsData || []; FoolAnalyticsData.push({ eventType: “ArticlePitch”, contentByline: “Lee Samaha”, contentId: “cms.133208”, contentTickers: “”, contentTitle: “Which Stocks Will Win From the War on Coal?”, hasVideo: “False”, pitchId: “350”, pitchTickers: “”, pitchTitle: “”, pitchType: “”, sfrId: “” });

The article Which Stocks Will Win From the War on Coal? originally appeared on Fool.com.

var ord = window.ord || Math.floor(Math.random() * 1e16);

document.write(‘x3Cscript type=”text/javascript” src=”http://ad.doubleclick.net/N3910/adj/usdf.df.articles/articles;sz=5×7;ord=’ + ord + ‘?”x3ex3C/scriptx3e’);

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends Emerson Electric. The Motley Fool owns shares of General Electric Company. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 – 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.

(function(c,a){window.mixpanel=a;var b,d,h,e;b=c.createElement(“script”);

b.type=”text/javascript”;b.async=!0;b.src=(“https:”===c.location.protocol?”https:”:”http:”)+

‘//cdn.mxpnl.com/libs/mixpanel-2.2.min.js’;d=c.getElementsByTagName(“script”)[0];

d.parentNode.insertBefore(b,d);a._i=[];a.init=function(b,c,f){function d(a,b){

var c=b.split(“.”);2==c.length&&(a=a[c[0]],b=c[1]);a[b]=function(){a.push([b].concat(

Array.prototype.slice.call(arguments,0)))}}var g=a;”undefined”!==typeof f?g=a[f]=[]:

f=”mixpanel”;g.people=g.people||[];h=[‘disable’,’track’,’track_pageview’,’track_links’,

‘track_forms’,’register’,’register_once’,’unregister’,’identify’,’alias’,’name_tag’,

‘set_config’,’people.set’,’people.increment’];for(e=0;e<h.length;e++)d(g,h[e]);

a._i.push([b,c,f])};a.__SV=1.2;})(document,window.mixpanel||[]);

mixpanel.init(“9659875b92ba8fa639ba476aedbb73b9”);

function addEvent(obj, evType, fn, useCapture){

if (obj.addEventListener){

obj.addEventListener(evType, fn, useCapture);

return true;

} else if (obj.attachEvent){

var r = obj.attachEvent(“on”+evType, fn);

return r;

}

}

addEvent(window, “load”, function(){new FoolVisualSciences();})

addEvent(window, “load”, function(){new PickAd();})

var themeName = ‘dailyfinance.com’;

var _gaq = _gaq || [];

_gaq.push([‘_setAccount’, ‘UA-24928199-1’]);

_gaq.push([‘_trackPageview’]);

(function () {

var ga = document.createElement(‘script’);

ga.type = ‘text/javascript’;

ga.async = true;

ga.src = (‘https:’ == document.location.protocol ? ‘https://ssl’ : ‘http://www’) + ‘.google-analytics.com/ga.js’;

var s = document.getElementsByTagName(‘script’)[0];

s.parentNode.insertBefore(ga, s);

})();

Read | Permalink | Email this | Linking Blogs | Comments

Source: Investing